As always, the content below is meant as general information to give you a better understanding of this topic, and is subject to our terms and conditions. You should seek appropriate personalised financial advice from a qualified professional to suit your individual circumstances. We are happy to help you arrange this :)

How does a mortgage work?

A mortgage is essentially a loan that you take out with a bank, or other financial institution, for the purposes of buying property. While banks aren’t the only ones who offer mortgages, for simplicity we’re going to refer to them when we talk about lenders for the rest of this guide.

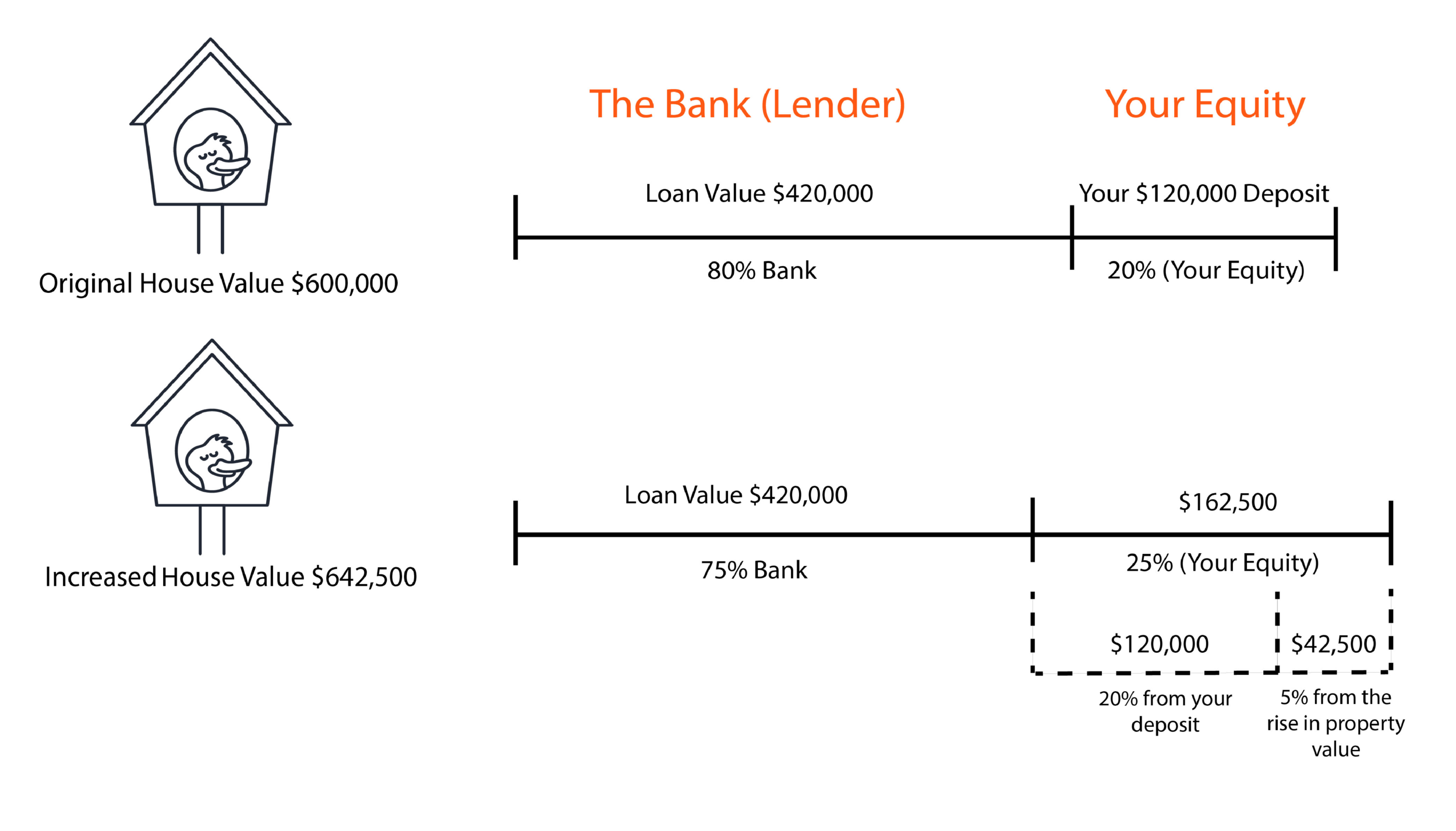

A mortgage example: say you want to buy a home for $600,000, but only have access to $120,000 in cash. You can apply to the bank to borrow the remaining $480,000, and pay the rest off over time. The bank benefits from this loan by charging you interest on the $480,000 at an agreed rate, until you pay it back.

There are some key terms to know in relation to mortgages:

Deposit: The amount of money you have available to put towards buying the home. Often made up of cash and the money in your KiwiSaver account. In the above example, this is the $120,000.

Equity: This is how much of the property you actually own, based on its market value. It is usually referred to as a % figure. So from the example above, on the day of purchase you had 20% equity (your $120,000 deposit) in that $600,000 property. This means the bank’s loan represents the other 80% of the property’s value.

Interest Rate: Each year, the bank charges you a percentage of the amount you have borrowed. The % rate they charge is called the ‘interest rate’ - at the time of writing, mortgage interest rates varied from about 3.85% to 6.80% for most banks.

Repayments: The money you regularly give to the bank to pay off your loan. These are usually weekly, fortnightly, or monthly payments. Each repayment has a portion that is interest (based off the % amount mentioned above) and a portion that is principal (money that goes towards actually paying off the lump sum you borrowed). The more you can chip away at the principal, the more equity you have, and the less interest you will pay in the long run.

Increasing your equity

As the value of your property increases, so does the equity you hold in the property. In simpler terms: if your property goes up in value over time, you will own a bigger percentage of the property compared to the bank.

Again using the above example, let’s say $600k property magically jumped in value by $42,500 the day after you purchased it - and is now worth $642,500. You would now own 25% of the property instead of the 20% because you benefit from the property’s value increasing over time, not the bank. The bank’s $420k loan now only represents 75% of the property’s value, instead of the 80% yesterday.

This is a general example only, and does not take into account interest, inflation or repayments over time etc.

Interest rates

When it comes time to take out a mortgage, interest rates play a big part in deciding who to borrow money from. Different banks (and other lenders) offer different interest rates, depending on whether you want to ‘float’ or ‘fix’ - more on this later.

It’s important to note that interest rates can change over time. Although it hasn’t changed much in recent times, what the banks are offering in April, may be different to rates they are offering in October. This is because of something called the ‘OCR’.

Without going into too much detail, the ‘OCR’ (or the Official Cash Rate) is an interest rate set by the Reserve Bank of New Zealand. They use it to regulate our economy, and control inflation.

It may sound odd, but banks actually borrow money too. The OCR is the ‘wholesale rate’ of borrowing money - which the banks have access to. So, if the OCR goes up, and the banks have to pay more interest when they borrow money, our mortgage interest rates will probably go up too. If they OCR goes down, the mortgage interest rates on offer from the bank will usually follow.

Different types of mortgages

Here we’re going to focus on the two main types: fixed and floating mortgages.

Floating-Rate Mortgages - Here, your interest rate will change over time. This is great if your bank’s floating interest rate goes down, not so great if it goes up.

The main benefit of opting for a floating rate is flexibility. There are no penalties for paying off lump sums of your mortgage. This is great if you are paid in irregular amounts, for example monthly commissions or bonuses.

The tradeoff is that historically, floating rates have been higher than fixed rates. So you need to evaluate your situation, and decide whether the added flexibility is worth the higher interest rate.

Fixed-Rate Mortgages - For this type of home loan, you lock in your interest rate and your repayments for a certain period of time.

This is great for budgeting. You can usually lock in an interest rate for a period of time between 6 months - 5 years, and you will know exactly how much money you need to pay for that fixed period.

The downside here is that if you want to pay off more (or all) of your loan outside of your regular repayments, the bank will charge you what is called a ‘break fee’. This fee is usually calculated by taking into account how much interest the bank is going to ‘miss out on’ as a result of you breaking the fixed term.

Having said that, some banks will give you a little leeway, and let you pay off a bit more than you originally agreed when you set up the fixed term. For example, the bank may let you increase your fortnightly repayments by 20% - and all of this extra money will go to pay off the principal, because the interest rate is already locked-in.

Float or Fix? - As with pretty much everything in the financial world, it depends on your circumstances. But one key thing to remember is that you can have the best of both worlds. Most lenders will let you fix part of your loan, and float the other. And remember, if you don’t like the way interest rates are heading, you can move some or all of your debt from floating to fixed.

If you have any questions you would like answered, please flick us an email hello@ducksinarow.nz